Running a tree service business in Canada comes with plenty of challenges – from bad weather to heavy equipment and working at heights. Every job has risks, and without the right insurance, one accident can cost more than money. In this line of work, it is best to “nip problems in the bud” before they turn into bigger troubles.

Insurance is not only about paperwork. Its main purpose – safety. It protects your crew, your gear, and your life. Now, insurance rules vary by region, so if you know them you can save yourself from fines or shutdowns.

But we should be real – figuring out insurance for a tree service business can feel like hacking through a forest without a map. Do you really need all those add-ons? Is the coverage you have enough to keep your crew and equipment protected? How to balance cost with peace of mind?

We will break it down so you can focus on growth, not risks.

Why Tree Service Insurance Matters for Your Business

If you owned a tree service business in Canada, you would deal with workers climbing trees with chainsaws and using heavy equipment near homes, businesses, and power lines. One mistake could mean a fall, a broken machine, or injuries from falling branches. That’s why arboriculture would be one of Canada’s most dangerous trades.

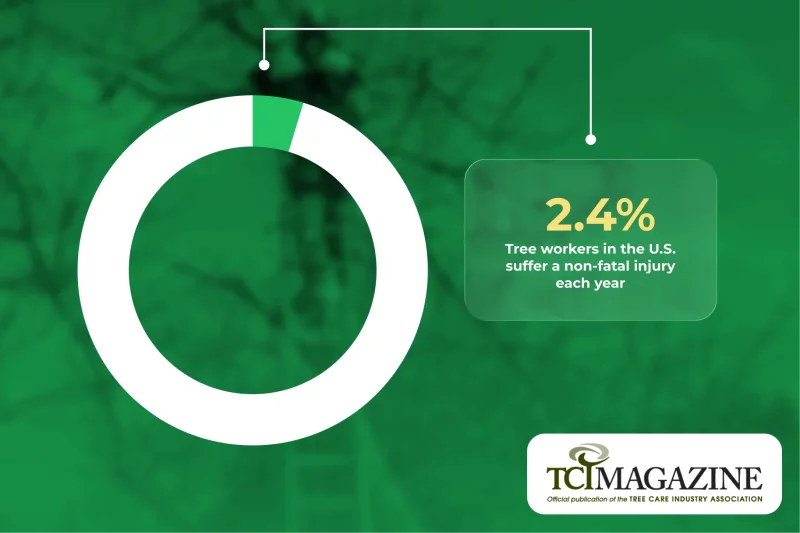

According to Tree Care Industry Magazine, about 2.4 out of every 100 tree workers in the U.S. suffer a non-fatal injury each year. Even one accident can cause serious harm, damage property, or worse – and that can mean costly lawsuits, medical bills, and big disruptions for a business.

Insurance protects your tree business from costly claims, such as property damage exceeding $100,000 or worker injuries. It also helps cover medical bills and lost wages while building client trust. Cases like a 2024 Ontario arborist facing a $200,000 claim show why strong coverage is essential.

Tree Service Insurance Requirements by State and Operation Type

Canada has no federal law requiring tree service insurance. Each province sets its own rules through workers’ compensation boards, like WSIB in Ontario or WorkSafeBC in British Columbia. Employers must have workers’ comp.

Sole proprietors need it for public contracts or municipal work. Breaking the rules can mean fines or losing the right to operate. General liability insurance is not mandatory everywhere. Still, most clients and cities require it, usually from $1–2 million. Rules vary. BC and Alberta focus on heavy equipment work. Ontario and Quebec focus on urban care. Atlantic provinces have higher premiums due to storms.

The next stage – briefly walking through main tree service insurance requirements.

Ontario (WSIB)

Workers’ compensation is mandatory for all employers, and tree services fall under forestry codes. Contractors have to carry general liability insurance, with Toronto requiring proof for permits. In 2025, the average WSIB rate is $1.25 per $100 of payroll, and contractors generally need $2 million in liability coverage. Tree removal usually requires WSIB clearance plus a $5 million umbrella policy for commercial jobs, trimming calls for $1–2 million in liability to cover debris claims, and stump grinding needs extra protection due to heavy equipment use.

British Columbia (WorkSafeBC)

Workers’ compensation is mandatory for all tree services, with WorkSafeBC rates averaging $1.55 per $100 of payroll due to the industry’s high risk. Most BC municipalities require at least $2 million in general liability coverage for permits, and Vancouver requires proof for removals. Standard residential tree removal typically needs $2 million in CGL, while high-risk utility or commercial work often requires $5 million or more in CGL or umbrella coverage. Trimming generally calls for $2 million in coverage, and stump grinding requires both commercial auto service insurance for transport and an Equipment Floater for the grinder.

Alberta (WCB)

Workers’ compensation is mandatory for employers, and sole proprietors also need it when working as subcontractors. The average WCB rate is $1.41 per $100 of earnings, but arborists, classified under Logging/Timber Management, typically pay closer to $2.89 due to higher risk. Insurance needs vary by job and location: Calgary requires $5 million in general liability, tree removal usually calls for $2–$5 million because of its high-risk nature, trimming generally needs $2 million, and stump grinding requires extra coverage for valuable equipment like grinders and chippers, since theft and damage risks drive up rates.

Quebec (CNESST)

Workers’ compensation covers forestry work, and requirements vary by job type and location. In 2025, the average CNESST rate is $1.48 per $100 of payroll, though forestry rates are significantly higher. Liability certificates are required for all work, with many arborist groups demanding $2 million in GL; in Montreal, proof of CNESST and GL is mandatory. Tree removal typically requires $2–$5 million in GL plus a Certified Arborist Report, trimming needs $2 million, and stump grinding requires an Equipment Floater for valuable gear and often pollution coverage for spill risks. Other provinces have similar rules, with Workers’ Compensation always required and $1–$2 million in GL standard, varying by risk.

Essential Tree Service Insurance Policies

Tree service work in Canada carries high risks, so proper insurance is essential to protect your business, workers, and clients.

General Liability Insurance

It protects your business from third-party claims – like injuries or property damage – and covers legal costs, which can exceed $50,000 per claim. GLI includes:

-

Bodily injury – for example, if a passerby gets hurt by falling debris during pruning

-

Property damage – for instance, if a felled tree branch cracks a client’s vehicle or roof

Average annual costs in 2025

For small tree service businesses with 1–5 employees and under $500,000 in revenue, a $2 million liability policy usually costs $540–$2,000. Brokers often start quotes around $500–$750. Larger companies with 10+ employees and over $1 million in revenue pay $2,500–$12,000. Coverage ranges from $2 million for small firms to $5 million or more for larger ones. In addition, bundling policies can save 10–15%.

Workers’ Compensation Insurance

Workers’ compensation is mandatory in all Canadian provinces and territories for businesses with employees. It also includes tree services. Bodies such as WSIB in Ontario, WorkSafeBC in British Columbia, WCB in Alberta, and CNESST in Quebec manage it. In some provinces, like Alberta, the law does not require sole proprietors to have coverage, but authorities often require it for permits, contracts, or subcontracting.

This coverage protects employees from injuries related to falls, chainsaws, or heavy equipment, covering medical expenses, lost wages (typically 75–90% of net earnings, subject to provincial caps such as $117K in Ontario for 2025), and death benefits.

Non-compliance carries severe penalties, including fines up to $500,000 in Ontario, $100,000 in Nova Scotia plus full claim reimbursement, and over $700,000 in British Columbia along with possible stop-work orders.

Commercial Auto Insurance

Commercial auto insurance covers vehicles used to transport crews, tools, and equipment, including company-owned, leased, or rented trucks such as pickups, chippers, and bucket trucks. It protects against accidents, theft or vandalism, and liability claims for injuries or property damage, which personal auto policies don’t cover. Typical policies include $2 million liability, collision/comprehensive coverage, and optional cargo or pollution protection.

Common claims in tree service

Common claims in tree service include load shifts that cause collisions or falling debris, rollovers from uneven terrain or high loads, property damage from protruding equipment, theft of vehicles or tools, and weather-related incidents such as hydroplaning.

Approximate annual costs per vehicle in 2025

-

Standard trucks: $1,800–$3,500

-

Specialized equipment trucks: $3,000–$6,000 due to higher risks and repair costs

-

Fleets of five or more vehicles: discounts of 10–20% available through particular providers

Equipment and Tools Coverage

Inland marine insurance protects mobile gear like chainsaws, stump grinders, and chippers on site, in transit, or in temporary storage, covering theft, fire, vandalism, accidents, and weather damage. Optional add-ons can include rental reimbursement.

In 2025, it typically costs 2–4% of the equipment’s total value annually, with high-value items like a $50,000 chipper at about 1–2% and smaller tools up to 4%, depending on province and risk.

Professional Liability Insurance

Professional liability insurance (E&O) in Canada protects tree service businesses from claims of negligence, errors, or omissions in advice or services. Unlike general liability, it covers financial losses to clients, including legal costs, settlements, and judgments.

It’s important when offering services like tree health assessments, risk evaluations, pruning advice, or pest management plans. Often required by associations like Arboriculture Canada, E&O is highly recommended for ISA-certified arborists to protect against personal liability.

Potential claim scenarios in Canada

-

Faulty health assessment. An arborist inspects a mature oak in Toronto and deems it stable, but months later decay causes a branch to fall on a neighbor’s garage, causing $40,000 in damages. The client sues for negligent evaluation.

-

Incorrect treatment advice. Improper pruning advice for a birch tree in Vancouver causes its decline and death, costing the homeowner $15,000. The claim alleges professional misconduct.

-

Missed deadline or error in service. Failing to complete a tree risk assessment before a home sale in Ontario leads to hazards being discovered later, resulting in a $25,000 lawsuit for breach of contract.

-

Overlooked hazard on-site. During a trimming job in Calgary, an adjacent untreated tree falls and damages a client’s vehicle. Even without working on it, the arborist could be liable for not warning the owner of the risk.

Tree Service Insurance Costs: What to Expect

Tree service insurance costs in Canada depend on several key factors:

-

Business size. More employees, vehicles, and higher revenue increase premiums.

-

Location. Provincial rules, urban density, and weather risks matter. For example, Ontario and storm-prone Atlantic provinces like Nova Scotia often have 15–25% higher premiums due to more frequent claims.

-

Services offered. High-risk activities, such as aerial removal near utilities, increase rates.

-

Claims history. Past incidents can raise costs by 20–50% for 3–5 years.

-

Safety measures. A clean record and certifications (e.g., from Arboriculture Canada) can lower rates.

Larger firms pay more due to more vehicles, equipment, and higher risks. Small teams or sole proprietors have lower rates. Heavy machinery or big contracts need higher coverage ($2–5 million), raising premiums.

Typical annual premiums for comprehensive coverage:

-

Small operations: $7,000–$15,000

-

Large operations: $80,000+

Sample ranges (based on $1–2 million general liability limits, standard deductibles, and average provincial rates):

| Business size | General liability | Workers’ comp (payroll-based) | Commercial auto (per vehicle) | Total annual estimate |

|---|---|---|---|---|

| Small (1–5 employees, $100,000–$500,000 revenue) | $600–$2,000 | $3,000–$6,000 ($2–$4 per $100 payroll) | $1,800–$3,000 | $7,000–$15,000 |

| Medium (6–20 employees, $500,000–$1 million revenue) | $3,500–$6,000 | $10,000–$20,000 | $3,000–$5,000 | $40,000–$80,000 |

| Large (20+ employees, $1 million + revenue) | $12,000+ | $25,000+ | $5,000+ | $80,000+ |

How to Save on Tree Service Insurance Without Losing Coverage

Tree service businesses in Canada can cut insurance for arborist costs by 10–30% while maintaining essential coverage like general liability and workers’ compensation. Then, we have to review some key strategies:

-

Policy bundling: combining general liability, property, and tools coverage can lower costs by 10–15%.

-

Safety programs: Arboriculture Canada or WorkSafeBC-approved training may reduce workers’ comp rates by 5–15%.

-

Higher deductibles: increasing deductibles can cut premiums by 10–25%, though a claims reserve is advisable.

-

Seasonal adjustments: reducing coverage in slower seasons can save 10–25% while retaining core protection.

-

Annual payment & market review: paying yearly and comparing quotes from multiple brokers can yield 10–20% in savings.

Common Tree Service Insurance Mistakes to Avoid

As we can see, tree service businesses face unique risks, and avoiding common insurance mistakes can save time, money, and trouble. Below, you can find details about what mistakes you may do and how to avoid them:

| Insufficient coverage limits

|

Choosing coverage below $2 million for General Liability is a severe mistake. In urban centers (Vancouver, Toronto, Montreal), property values are high, and tree claims (damaging a house, car, or fence) frequently exceed $100,000. $2–$5 million limits are standard for professionals and required by most commercial clients.

|

| Ignoring subcontractor insurance | This is a major liability in Canada. If a contractor (even an independent operator) is injured and does not have their own active WCB/WSIB/CNESST coverage, the hiring business is often deemed the employer for that job and becomes liable for the claim, fines, and back premiums. Prevention must include verifying their “Clearance Letter” before work begins and naming your tree business as Additional Insured on their General Liability policy. |

| Failing to document safety practices | Documentation is key to both mitigating claims and securing premium incentives. Provincial workers’ compensation bodies like WSIB reward businesses with documented safety programs (e.g., the Health and Safety Excellence Program in Ontario) with premium rebates and better rates over time. Lack of records means losing those financial benefits and potentially having a claim denied or contested. |

| Using personal policies for business | A Personal Auto Policy will explicitly exclude any vehicle or trailer used to haul commercial equipment (like chippers, stump grinders, or logs) for a fee. This immediately voids coverage in the event of an accident during transport. A Commercial Auto Policy and Inland Marine/Tools & Equipment Floater are mandatory. |

| Overlooking policy exclusions | Standard Commercial General Liability (CGL) policies are written to exclude the highest risks of the tree service trade unless specific endorsements are added. |

Choosing the Right Insurance Provider for Tree Services

When choosing insurance for your tree service business in Canada, pick providers who understand arborist risks like aerial work, heavy equipment use, and provincial workers’ compensation rules. Avoid generic policies that exclude tree-specific coverage. Look for brokers or insurers with arborist expertise or Arboriculture Canada partnerships.

Recommended providers:

-

Morison insurance – Ontario-focused, arborist-specific endorsements

-

Zensurance – Nationwide, fast online quotes for liability and tools coverage

-

Insurance Hero – Competitive rates for tree removal companies

-

AMC insurance – Comprehensive packages including stump grinding and pruning

Key questions for agents:

-

What experience do you have with arborist businesses and high-risk work like tree felling near utilities?

-

How do your policies work with workers’ compensation boards (WSIB, WorkSafeBC)?

-

Can you add endorsements for exclusions such as pollution liability or inland marine coverage?

-

Do you offer discounts for Arboriculture Canada safety certifications or seasonal adjustments?

How to Compare Policies Effectively

Get quotes from at least three providers and share details about your business: revenue, employees, and services. Compare:

-

Coverage limits: $2–5 million GL recommended

-

Deductibles: $500–$2,000

-

Premiums: Check bundling options for 10–15% savings

-

Claims process: Look for under 24-hour response

-

Review policy wording for tree-specific coverage and additional insured options

-

Renew annually to benefit from a clean claims history

FAQ

Is general liability enough for tree services?

No, general liability alone is not enough for tree services in Canada. It covers third-party injury and property damage (e.g., a branch hitting a car) but not employee injuries (covered by WSIB/WorkSafeBC/CNESST) or equipment damage (requiring Tools & Equipment coverage). Most clients and municipalities also require higher limits ($2–$5 million), so policies should be bundled for full protection.

Does homeowners insurance cover tree work?

No. Homeowners insurance in Canada excludes commercial tree work, so arborists are personally liable for damages or injuries. A client’s policy may cover their own property but not your business liability (e.g., crane damage). Tree services need Commercial General Liability and other coverage to avoid major out-of-pocket costs.

Do I need different insurance for residential vs. commercial tree services?

Yes. Commercial tree services usually need higher General Liability limits ($2–$5 million) versus $1–$2 million for residential. They also often require added coverage like Pollution Liability and Professional Liability, especially for work near utilities or public spaces.

How much tree service insurance coverage do I really need?

Most Canadian tree services need $1–$2 million in General Liability (up to $5 million for commercial/municipal work), Workers' Compensation, and $50,000–$200,000 in Equipment Coverage. Exact needs depend on revenue, job risks, and provincial rules, so a specialized broker is key.

What happens if my subcontractors don’t have proper insurance?

If subcontractors lack proper coverage (e.g., $2 million General Liability, WSIB/WCB/CNESST clearance), you can be liable for their accidents, damages, fines, and claims. Always verify their service insurance, require your tree business as Additional Insured, and confirm clearance with the relevant provincial board.

Is workers’ compensation mandatory for all tree service businesses?

Yes. Workers’ Compensation is mandatory in Canada for tree service businesses with employees, and in some provinces (e.g., Ontario, BC) also for sole proprietors in construction. Non-compliance risks heavy fines and stop-work orders; optional coverage is available in other sectors.

Can I get seasonal tree service insurance to save money?

Yes. Seasonal adjustments can cut premiums 10–25% by scaling back or suspending unused coverage, but core liability and Workers’ Compensation must stay active. Always notify your broker to avoid gaps or penalties.

Final Thoughts: Protecting Your Tree Service Business for the Future

Good insurance is essential for a safe and lasting tree service business in Canada. It protects you from major risks – like costly property damage or worker injuries. General liability, workers’ compensation, and equipment coverage help your business handle accidents, legal claims, and penalties while keeping clients’ trust. As rules and risks change, review your policies yearly and work with arborist-focused brokers like Zensurance or Morison Insurance to ensure you’re fully covered.