Tree removal businesses need at minimum: general liability ($1M+ coverage), workers' compensation, and commercial auto. Add inland marine for equipment, professional liability if you provide tree assessments, and an umbrella policy for high-value jobs. Tree service is classified as high-risk – expect to pay more than general contractors and always verify your policy explicitly covers “tree work”, not just landscaping.

Why Tree Removal Insurance Is a Category of Its Own

If you run an arborist business, you already know: a tree is tons of weight hanging over homes, power lines, and people. One wrong cut can cost you everything.

Tree work remains one of the deadliest trades, with a fatality rate historically around 110 per 100,000 workers – dozens of times higher than average. Falls, falling limbs, power lines, and chipper accidents aren’t theory; they’re your weekly reality.

That’s why tree removal insurance and tree service insurance are in a category of their own. Generic landscaping policies often exclude real tree removal or elevated work. Clients demand a certificate of insurance that explicitly says “tree work,” not just “landscaping”. Without it, you’re exposed.

For arborist business insurance, start with:

-

General liability insurance tree service ($1M+ per occurrence)

-

Workers comp for arborists

-

Commercial auto insurance tree company

Smart operators also add inland marine for equipment, professional liability for assessments, and an umbrella for big jobs. Tree service insurance cost per month is higher than for typical contractors – because the risk is higher. ISA-certified owners often earn discounts.

The 5 Core Insurance Policies for Tree Service Businesses

Your guys don’t trim hedges – they take down trees that can crush roofs, cars, and careers in seconds. Here are the five essential insurance policies every tree service business needs in 2026 to protect your crew, your equipment, and your company.

1. General Liability

This is your first line of defense when things go wrong on the job. A falling branch punches through a client’s roof, a piece of debris dents their car, or a bystander gets hit by flying chips – general liability insurance tree service pays for the property damage and bodily injury claims from third parties.

Most arborist businesses should carry at least $1 million per occurrence. For commercial jobs, municipal contracts, or high-value properties, clients routinely demand $2M–$5M. Don’t skimp here – many bids get rejected without the right limits on your certificate of insurance.

Because tree service is considered high-risk, standard insurance carriers often won’t touch it. Your general liability is frequently placed in the Excess & Surplus (E&S) market. That means higher premiums, stricter underwriting, and fewer carriers willing to write the policy.

In 2026, expect general liability insurance tree service to run roughly $130–$150 per month on average for $1M coverage (around $1,500–$1,800 annually), though it can be lower for small operations with clean records or higher depending on your location, crew size, and claims history.

2. Workers' Compensation

When one of your climbers takes a fall or gets tangled in rigging, workers’ comp is the policy that actually pays the medical bills, lost wages, and rehab – without dragging you or your business into a lawsuit. In this industry, it’s not optional – it’s often the single biggest insurance expense because the injury risk is genuinely extreme.

-

Covers: medical bills, lost wages, rehabilitation, and disability benefits if a crew member is injured (or killed) on the job.

-

Required by law in most states as soon as you have even one employee (some states require it even for owners in certain cases).

-

NCCI class code 0106 applies to most arborists and tree trimmers – this is the specific code for tree pruning, trimming, repairing, and removal operations.

Workers’ comp is typically the largest line item for tree service companies due to the high-risk nature of the work. In 2026, expect average costs around $180–$220 per month (or $2,200–$2,700 annually), though this can vary significantly by state, payroll size, and claims history. ISA certification and a documented safety program can help lower your experience modification factor and reduce premiums.

Pro tip: Never try to “save money” by skipping workers’ comp or misclassifying your crew. A serious injury without proper coverage can personally bankrupt you.

3. Commercial Auto

Your trucks, chipper trailers, and bucket trucks are on the road every day hauling heavy equipment and crews to job sites. When one of them gets into an accident, a commercial auto insurance company covers liability, physical damage to your vehicles, and medical costs – things your personal auto policy won’t touch.

This coverage is required in most states for any business-owned vehicles. If your crew uses rented equipment or drives their own trucks to jobs, make sure you add Hired and Non-Owned Auto (HNOA) coverage – it fills the dangerous gaps that can otherwise come straight out of your pocket.

In 2026, expect commercial auto to cost roughly $150–$220 per month on average for a typical tree service fleet (higher for bucket trucks or multiple vehicles), depending on your state, driving records, and how much mileage you put on the road.

4. Inland Marine (Tools & Equipment)

Your chainsaws, chippers, stump grinders, climbing gear, and rigging equipment are some of the most expensive assets in your business – and they’re constantly moving between jobs, trucks, and storage. Inland marine insurance (also called equipment or tools coverage) protects them against theft, damage, or loss whether they’re on a job site, in transit, or sitting at your yard.

This coverage is especially critical for tree service companies because standard property insurance usually stops at your shop door. A stolen $15,000 chipper or a damaged aerial lift can set you back hard if you’re not properly covered.

In 2026, inland marine for a typical arborist setup averages around $50–$80 per month (roughly $600–$1,000 annually), depending on the total value of your equipment. Many small-to-mid size operations fall near the $57/month mark.

Pro tip: Schedule high-value items like chippers and grinders separately for better limits and broader protection.

5. Professional Liability (Errors & Omissions)

You climb the tree, make the call, and tell the homeowner or property manager whether to keep or remove it. If that recommendation later goes wrong – the tree falls and causes major damage – the client can sue you for giving bad advice. That’s where professional liability (also called Errors & Omissions) steps in.

It covers claims that your tree assessment, report, or recommendation caused financial loss or property damage. This coverage becomes especially important if you’re ISA-certified, writing formal reports, doing consulting work, or bidding on municipal or commercial contracts. Most standard general liability policies do not include professional liability, so don’t assume you’re covered. Adding it gives you real protection when your expertise is on the line.

Optional but Recommended: Umbrella & BOP

As your jobs grow bigger – think crane-assisted removals, multi-day commercial projects, or city contracts – your standard liability limits can quickly run out. This is where two smart add-ons come into play to give you extra breathing room when the stakes are highest.

| Coverage | What It Does | Best For | Typical Cost (2026) |

|---|---|---|---|

| Umbrella Policy | Extends your liability limits across general liability, commercial auto, and employer’s liability | Large-scale jobs, crane work, municipal bids, high-value properties | $40–$120 per month (for $1M extra coverage) |

| BOP (Business Owner’s Policy) | Bundles general liability with commercial property protection in one package | Businesses with a yard, shop, office, or stored equipment | $180–$200 per month |

Completed operations coverage is another key detail worth double-checking. It protects you against claims that surface weeks or months after the job is finished – for example, if a tree you removed later fails and causes damage. Most general liability policies include it, but always confirm the wording explicitly lists tree service work.

Pro tip: Pairing an umbrella with your core policies often delivers the best bang for your buck on high-risk tree jobs.

How Much Does Tree Service Insurance Cost?

Pricing tree service insurance in 2026 feels like guessing the weather – it changes depending on where you operate, how many crews you run, your safety record, and the types of jobs you take. A small operation with clean claims might pay under $400 a month total, while a larger fleet with multiple vehicles and high-value equipment can easily top $800–$1,200 monthly. The real key? Bundling policies (especially through a BOP or combining GL + workers’ comp + auto) often delivers 19–27% savings compared to buying everything separately.

Here are realistic monthly cost ranges for the main coverages most arborist businesses need:

-

General Liability – $130–$150 per month (for $1M per occurrence). Higher limits or E&S market placement can push it up.

-

Workers’ Compensation – $180–$220 per month on average. This one fluctuates the most based on your total payroll and state rates.

-

Commercial Auto – $150–$210 per month for a basic fleet (trucks + trailers). Bucket trucks or poor driving records drive the price higher.

-

Inland Marine (Tools & Equipment) – $50–$80 per month, depending on the total insured value of your chainsaws, chippers, and grinders.

-

Umbrella Policy – $40–$120 per month for an extra $1M–$5M in liability protection.

-

Professional Liability (E&O) – $60–$90 per month if you provide assessments and written reports.

Business Owner’s Policy (BOP) – $180–$200 per month when bundling GL + property — often the smartest way to save.

What Drives Your Premium Up (and How to Bring It Down)

Several factors can push your tree service insurance cost per month significantly higher – or help you pull it back down. Underwriters look closely at the real hazards your crews face every day, so understanding these levers gives you real control over arborist business insurance expenses.

What tends to drive premiums higher:

-

Working near power lines or using cranes on complex removals

-

Taking on municipal contracts or large commercial projects

-

Running bigger crews with higher payroll

-

Expensive equipment fleet and frequent storm-prone work

-

Any past claims or losses on your record

What can bring your costs down:

-

ISA certification insurance discount – many carriers reward it because it signals lower risk

-

Full compliance with ANSI Z133 safety standards

-

Written, consistently followed safety programs and training records

-

Clean OSHA history with zero serious incidents

-

Paying premiums annually instead of monthly

-

Raising deductibles on inland marine insurance tree equipment for less expensive gear

ISA certifications and solid, documented safety procedures aren’t just nice-to-have marketing points – underwriters treat them as concrete proof that you run a tighter operation. That translates into measurable savings on general liability insurance tree service, workers comp for arborists, commercial auto insurance tree company, and the rest of your package.

Subcontractors and Insurance – a Common Trap

Growing your tree service operation often means bringing in subcontractors to handle overflow work or specialized jobs. But here’s a harsh reality many owners learn the hard way: if your sub has an accident or damages property, their mistake can land squarely on your shoulders – and your wallet.

This is one of the fastest ways arborist business insurance turns into an expensive headache. Even if you have solid general liability insurance tree service and workers comp for arborists, gaps with subcontractors can leave you fully exposed.

To stay protected:

-

Always demand a current certificate of insurance tree service from every subcontractor before they start work.

-

Make sure your company is listed as an additional insured on the tree service BOP business owner policy.

-

Verify that their coverage actually includes tree removal and tree work — not just generic landscaping.

Skipping this step is one of the most common (and costly) oversights for expanding tree care companies. A single uninsured sub incident can spike your tree service insurance cost per month and damage your claims history for years.

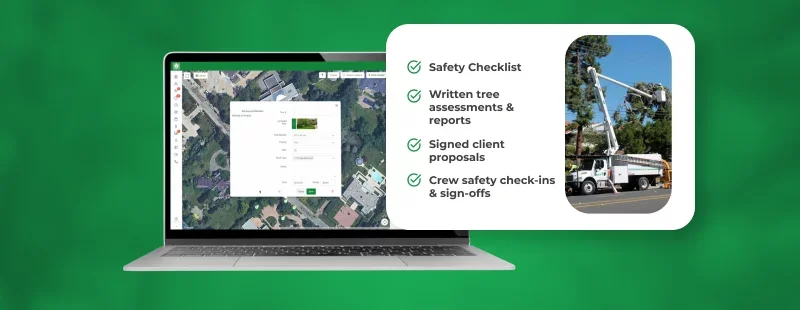

How Proper Job Documentation Reduces Insurance Risk

Strong documentation isn’t just paperwork – it’s one of the most effective ways to lower your insurance risk and strengthen your position when underwriters review your arborist business insurance. Carriers love seeing proof that you run a professional, well-managed operation rather than relying on memory and verbal agreements.

When every job has clear records – pre-work assessments, site photos, signed proposals, crew safety briefings, and post-job notes – you create a solid defense against disputed claims. This directly helps keep your tree service insurance cost per month more stable and can even improve your chances of better rates or fewer exclusions.

| Documentation Practice | How It Helps Your Insurance |

|---|---|

| Written tree assessments & reports | Shows due diligence and supports professional liability defense |

| Before-and-after site photos | Proves conditions at the time of work |

| Signed client proposals | Clarifies scope and reduces “you never told me” arguments |

| Crew safety check-ins & sign-offs | Demonstrates consistent safety culture to underwriters |

ArboStar’s CRM and job management tools make this process seamless for tree care businesses. From digital estimates and site photos to crew sign-offs and automatic reports, it builds a clean, professional paper trail that strengthens your insurance for tree service companies applications and helps protect against future claims disputes.

Better documentation doesn’t just reduce headaches – it often translates into real savings on general liability insurance tree service, workers comp for arborists, and the rest of your package.

Pro tip: Treat documentation as part of your safety program, not an afterthought. Underwriters notice the difference.

Conclusion

Insurance isn’t just another expense you check off once a year – it’s the silent partner that either shields your arborist business when storms hit, or quietly sinks it. In 2026, the smartest tree service owners treat tree removal insurance and tree service insurance as strategic tools, not afterthoughts. They price jobs with real risk in mind, demand proper coverage, and back everything up with airtight documentation.

Getting the right mix of general liability insurance tree service, workers comp for arborists, commercial auto, and the supporting policies isn’t about playing it safe – it’s about playing it smart. It’s what lets you take on bigger jobs with confidence instead of crossing your fingers.

At the end of the day, strong insurance paired with sharp operational habits is the difference between a business that weathers the next big claim and one that doesn’t.

Want to make your documentation bulletproof and your insurance profile stronger at the same time? Book a quick demo and see how ArboStar helps tree care crews capture job photos, safety records, client sign-offs, and everything else underwriters love to see – all in one clean, simple platform.

Your crews work hard up in the trees. Make sure your business is equally well protected on the ground.